I often wonder, what if Basel II capital accords had been in place prior to the Great Recession?

Could the devastating crisis fueled by the serial pops of credit bubbles rumbling through the dismal landscape of G20 principalities been avoided with better capital adequacy safeguards?

Could the precious Post Cold War peace dividend been preserved; had the fiduciaries of global solvency not toppled the dominoes of economic prosperity and political stability through extreme selfishness and irrational behavior?

Some economists assert that had the guidelines of Basel II been in place it would not have mattered. That may certainly be true, but one is still left to wonder if Systemically Important Financial Institutions (SIFI) had followed better governance frameworks the fissures emanating from the epicenter of the global economic meltdown would not have been as deep or as widespread.

The lessons learned from the crisis are being codified in the new governance frameworks of Basel III. Whereas previous Basel Accords focused on capital adequacy and loss reserves aligned to risk weighted assets and counterparty exposures, Basel III looks to strengthen capital adequacy by addressing liquidity and leverage risk in the banks capital structure. Basel III recognizes the primacy of mitigating the systemic risk concentrated in the capital structure of a SIFI and lesser designees, and the contagion threat it poses on its counterparties and the greater economy.

To ally solvency concerns, Basel III installs a leverage ratio and bolsters its Liquidity Coverage Ratio (LCR) which will require all banking institutions to increase its regulatory capital reserves of High Quality Liquid Assets (HQLA). An increase in HQLA reserves will raise the cost of capital for all financial institutions requiring it to raise its spreads on credit products.

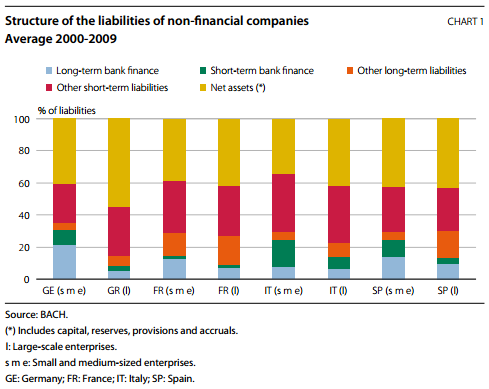

SMEs will be particularly affected by Basel III initiatives. SME’s are highly dependant on bank capital and credit products and remain highly sensitive to the cyclicality of macroeconomic factors. D&B’s Small Business Health Index reports that SME business failures in the US were in excess of 140,000 per month in 2013. The OECD reported that during 2012 over 800,000 EC SME’s closed shop in 2012.

Eurofact reported that 60% of all non-financial value add to the EC economy is attributable to SMEs. Though SMEs are generally recognized as principal economic drivers in both the developed and lesser developed economies; during the economic crisis SME’s were rationed out of the credit markets. Large capital infusions and accommodative monetary policy by the central bank authorities principally sought to bolster bank capital and inject liquidity into the faltering global banking system.

As such much of the low cost capital provided to banks did not trickle down to SMEs. Better returns were realized by deploying capital to investment partnerships, energy resource development, the acquisition of strategic commercial enterprises and underwriting speculative trading in the global security markets.

Little of the low cost capital found its way onto Main Street; driving the bifurcating wedge between the real and speculative economy. As a more conservative political landscape emerges from the wreckage of the economic calamity created by “elitist” financial institutions and “remote” Brussels based government bureaucrats, the cause of the SME is resonating in the rising voice of a middle class spoken with a distinct nationalist accent.

Politicians, legislators and advocacy groups are fully invested in the cause of the SME. Stakeholders are advocating more government involvement to underwrite and guarantee sponsored loans. In an era where government involvement in markets is under severe attack, political expediency and prudent economics coalesce to fund the incubation of SMEs. Even if greater government intervention is counterintuitive to laissez faire proclivities of the politically engaged, higher taxes would be required to fund the risk of capital formation initiatives. The securitization of SME loans is also a consideration; but aversion to leverage and the risk to encourage poor lending practices raise fears of creating yet another credit bubble.

The Government of Singapore recently rose its guarantee on SME loans to cover 70% of principal in response to the increase in cost of capital banks will charge as a result of Basel III. Spreads on SME loans are estimated to increase between 50 to 80 basis points. This rise in the cost of capital will allow banks to recoup Basel III compliance expenses associated with the segregation of regulatory capital requirements to service SME loan portfolios.

The risk premia on SME loans is justified by regulators because it guarantees the availability of credit through the business cycle. The financial health of SME’s are highly correlated to the vicissitudes of the business cycle. During times of cyclical downturns risk factors for SMEs are magnified due to the prevalence of concentration risk in products, regions, markets, client and critical macroeconomic factors germane to the SME’s business. Mitigation initiatives are inhibited due to liquidity constraints, resource depletion and balance sheet limitations. The closure of credit channels exacerbates this problem and Basel III risk premia pledges to fund SMEs through a trying business cycle.

To maintain profitability of SME lending, banks will enhance quality standards and haircut collateral margins; a potentially onerous demand since asset valuations remain severely distressed from the effects of the Great Recession. Banks will avoid SMEs with enhanced risk profiles, make greater use of loan covenants, expand fee based services and hike origination fees to protect margins and instill enhanced credit risk controls to minimize default risk.

As the strictures of Basel III take root within commercial banks alternative credit channels are opening to better match an SME’s credit requirements and market situation with a financial product that best addresses their business condition. D&B has initiated a timely capital formation initiative for SMEs. Access to Capital - Money to Main Street is an event tour that is bringing together regional providers of funding for SMEs and startups.

The economic recovery is combining with technology to energize innovations in SME funding options. Crowd-funding, micro-lending, asset financing, leasing, community bank loans, credit unions and venture capital channels are a few of the many options available for small business funding. Each channel offers distinct terms and advantages that match a funding option to the specific situation of an SME.

SME associations and advocacy groups are surfacing in the EU that seek to harness the residual capital created by SME failures. Second Chance and Fail2Suceed are initiatives that seek to harness the intellectual capital garnered by entrepreneurs in unsuccessful enterprises. It is a clear recognition that a great failure can be the mother of greater wisdom. This may augur well for the success of Basel III as it seeks to build on the shortfalls of its forebears to better protect the global banking system as it promotes the wealth of nations by equitably funding the growth of the global SME segment.

Sum2 offers a portfolio of risk assessment applications and consultative services to businesses, governments and non-profit organizations. Our leading product Credit Redi offers SMEs tools to manage financial health and improve corporate credit rating to manage enterprise risk and attract capital to fund initiatives to achieve business goals. Credit Redi helps SMEs improve credit standing to demonstrate creditworthiness to bankers and investors. On Google Play: Get Credit|Redi

Risk: SME, Basel III, commercial lending, political stability, economic growth, USA, EU, alternative credit channels, credit risk, global banking, business failure, OECD, SIFI

This article was originally released on DaftBlogger.